Easing by Appointment, Part 4

Domestic public enemy number one

I did not think that Dick Nixon could stick a knife into anyone in a cold, calculating fashion.

-Chairman Arthur Burns, January 8, 1974 (personal diary entry)

When we last visited Chairman Arthur Burns it was mid-1972 and he was doing his best to keep monetary policy from tightening prior to that year’s presidential election. Throughout 1972, Burns had appealed to wage and price controls as a preferrable alternative to tighter monetary policy. As seen in the excerpt below, he also spent a lot of time warning his colleagues about the political consequences of higher interest rates.

1973: Circling the Wagons

Over the course of 1972, the fed funds rate rose by about 150 basis points while inflationary pressure gathered strength. Only in 1973, when inflationary pressure was undeniable and the economy was in an extreme boom, did the Fed begin to tighten in earnest (Chart 1). Industrial production grew at a nearly 10% rate from 1972 through 1973 and homebuilding hit an all-time high in 1972 and nearly matched that level in 1973 (Charts 2 & 3). The economy turned red hot in 1972 and unemployment moved below 5% in early 1973.

In January 1973, Phase II (the mandatory portion) of the Nixon Administration’s price control scheme ended and Phase III (the voluntary portion) began. Inflation began to accelerate immediately, and Fed officials knew soon after that they had a problem on their hands. However, rather than definitively tightening policy, policymakers decided on a “middle ground” path that would accommodate some inflation but attempt to avoid a recession. As justification for their actions, FOMC members took the view that the federal government would go overboard in its fiscal response to a recession. The result was a cumulative fed funds rate increase of 500 basis points carried out in two pushes between January and November of 1973.

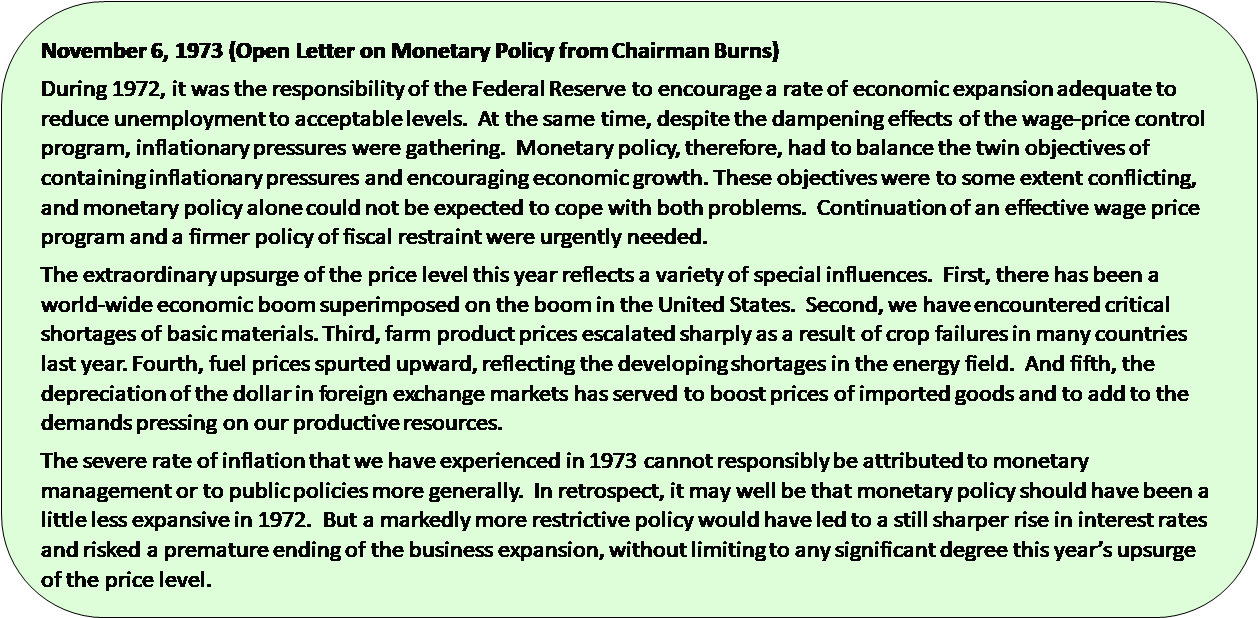

In September 1973, Senator William Proxmire of Wisconsin sent a letter to Chairman Burns demanding answers about the Fed’s conduct of monetary authority. Proxmire’s request for information was part of a larger effort to accuse Burns of using his position as Fed Chairman to influence monetary policy for the benefit of Richard Nixon’s 1972 presidential campaign. Whether Burns knew Proxmire’s ultimate goals when he sent his open response in November 1973 is unclear, but Burns was clearly circling the Fed’s wagons at this point. With inflation high and accelerating, but before the oil embargo had become a crisis, Burns disavows any Fed responsibility for the ongoing inflation.

In December 1973, the Saudis seized on the opportunity presented by a tight oil market to recoup purchasing power lost to Nixon’s dollar devaluations (Charts 4 & 5). The supply-side shock to the economy was recognized as likely to be enormous by Fed officials, but their expectations about the effects on demand were completely wrongheaded. In the December FOMC meeting, Burns said that “however painful it might sound, the System had no choice but to validate price increases that stemmed from supply shortages, because a failure to do so would probably results in a unacceptable declines in production, income, and employment.”

The similarity to the Fed’s reaction to COVID is shockingly similar, and the result has been the same inflationary mess. In December 1973, as in March 2020, fearful that a supply-side shock would cause panic among the ignorant wretches that make up their nation’s citizenry, Fed officials eased policy in a misguided attempt to stave off a depression that was never in the cards (Chart 6).

Keep reading with a 7-day free trial

Subscribe to Capitalist Pig Collective to keep reading this post and get 7 days of free access to the full post archives.