Easing by Appointment, Part 6

Only the Good Die Young

“...the general level of interest rates reached higher levels than I or any of my colleagues had really anticipated. That, in a perverse way, was one benefit of the new technique…I would not have had support for deliberately raising short-term rates that much.”

-Chairman Paul Volcker

In the summer of 1979, President Jimmy Carter faced a managerial crisis paralyzing his administration and an inflation crisis paralyzing the national economy. The crisis of management within his administration was very much of his own making. Carter, like most politicians, valued loyalty and tenacity among the political aides that worked at the White House. However, Carter also had grand notions about running a cabinet-style government where the various Secretaries act like independent Ministers with Portfolio, rather than taking political direction from the White House. Early in the administration Carter had said: “There will never be an instance while I am in office where the members of the White House staff dominate or act in a superior position to the members of the Cabinet.” Carter’s vision of a government free from political scheming was a grand one but was not long for the realities of Washington.

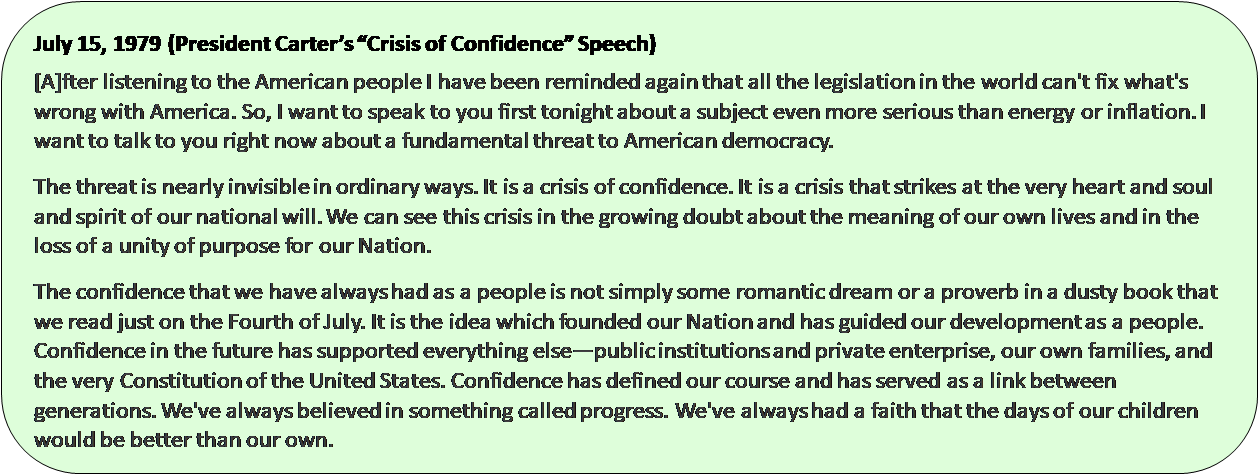

By mid-1979, with the Chairman of the Federal Reserve and the Secretary of the Treasury in open conflict over monetary policy and with voter confidence in his administration plummeting, Carter knew he needed to act if he wanted a second term. Part 2c discusses the political reshuffling that took place within the administration that led to G. William Miller moving from the position of Fed Chairman to Secretary of the Treasury. Carter’s efforts to salvage his presidency also involved an introspective look at the problems facing the country, with inflation taking most of the focus. The showpiece of Carter’s salvage effort was his July 15th speech on the “crisis of confidence” in the country, which popularly became known as the “malaise” speech.

As an American, to listen to the speech is to know deep and bitter disappointment. The first half of the speech is a masterpiece of language and empathy that raise the hopes of the listener. Carter’s words, and the feelings behind them, make clear that the President understood the nation faced difficult challenges and passionately wanted to solve them. The listener cannot help but feel stirrings of emotion, maybe this man can lead us out of the wilderness, maybe our best days are in front of us rather than behind. Unfortunately, the second half of the speech is merely the weak and watery plan of a bureaucrat, rather than the bold words of leadership that were needed.

The second half of the speech leaves the reader with the insurmountable question: Why in the wide-wide-world, Jimmy, did you ever take this job? The speech shows Carter to be a thoughtful and empathetic man who would do better serving on the search committee for presidential candidates. Public confidence was not improved by the speech, which is why it is remembered by a word describing the nation’s pitiful condition at the time, rather than in positive terms of national redemption and renewal. The task of bringing Great Inflation to its end would fall to others. This note tells their story.

Only the Good Die Young

Paul Volcker was not an unknown quantity when he became Chairman of the Federal Reserve Board on August 6th, 1979, having previously been the President of the New York Fed and the head of the so-called Volcker Working Group at the Treasury that secretly drafted plans to end gold convertibility of the dollar at the direction of President Nixon. Carter seems to have genuinely learned his lesson after selecting the highly partisan Miller as the prior Fed Chairman. In later interviews, Volcker disclosed that he was open with Carter that tighter monetary policy was needed to solve the inflation issue and he would pursue tighter policy if made Chairman. Indeed, Volcker had been at odds with Chairman Miller in FOMC meetings throughout the course of 1979 over the need for tighter monetary policy to combat inflation expectations, instead of caution in the face of potential recession.

Prior chairmen had pursued a policy of “gradualism”, which amounted to accommodation of inflation in the short-term balanced with sober promises for policy restraint that would disappear at the first sign of the next slowdown. Such a policy frequently resulted in the FOMC taking actions considered politically desirable and then afterwards trying to fit the actions into a twisted economic logic. In its annual report for 1979 the IMF discussed the disappointing results of gradualism, and the topic of expectations began to take center stage. Also noted in the report was the difficulty that economists were having in producing accurate forecasts in an environment of stagflation. The new chairman had also voiced frustration with gradualism, emphasized the importance of expectations, and rejected the idea of fine-tuning monetary policy based on econometric models, but he knew there was something lacking that would be needed to ensure success.

Keep reading with a 7-day free trial

Subscribe to Capitalist Pig Collective to keep reading this post and get 7 days of free access to the full post archives.