Easing by Appointment, Part 7

Endgame for the Great Inflation

Credit Interregnum

The Credit Control Act of 1969 had been passed to reinstate Presidential powers that existed during the Second World War, but that had lapsed during the 1950s. The Act allows the President to instruct the Federal Reserve to regulate and control “any or all extensions of credit”. It was added as an amendment to a more popular bill designed to put a ceiling on interest rates. The Act’s author’s highlighted credit controls as an alternative to general tightening of monetary policy. Nixon did not support the use of credit controls but signed the bill because he wanted to put a ceiling on interest rates.

President Carter initially resisted using credit controls on the justification that they were “inefficient and inequitable”. However, the Carter Administration began serious internal discussions about utilizing credit controls in 1979 in the face of rising inflation. Congressional Democrats began pushing more aggressively for credit controls in early 1980 with Carter’s Democratic primary opponent Sen. Ted Kennedy leading the charge. By March 1980, Carter had capitulated to the political pressure and rolled out a credit control program.

Carter rolled out the program with significant fanfare, but the credit controls were designed to be as toothless as possible. The guidelines advised banks on the allocation of credit to “useful” purposes and discouraged allocation of credit to unsecured consumer loans, mergers and acquisitions activity, speculative purchases, and commercial paper backstops. Changes to reserve requirements and new surcharge fees at the discount window caused confusion and turmoil in funding markets that did much more to restrain credit than the guidelines themselves.

By the end of March 1980, the first signs of recession resulting from the monetary tightening of the prior six months started to become apparent. In April and May, credit card applications and retail sales dropped off a cliff as many households enthusiastically embraced Carter’s new program. The sudden decline in demand compounded the effects of prior monetary tightening and by May 1980 Volcker was already talking with the Federal Reserve Board about dismantling the program. By June, credit creation was so weak that the controls were no longer binding, and the Board began dismantling the program.

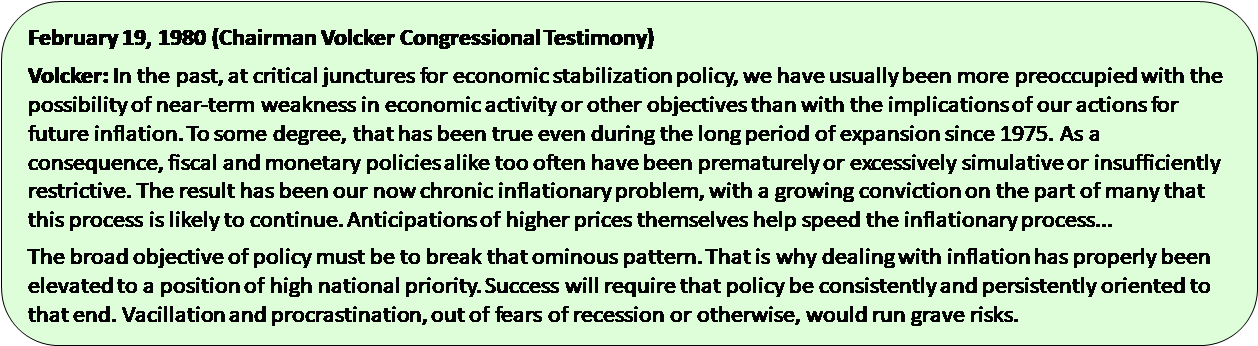

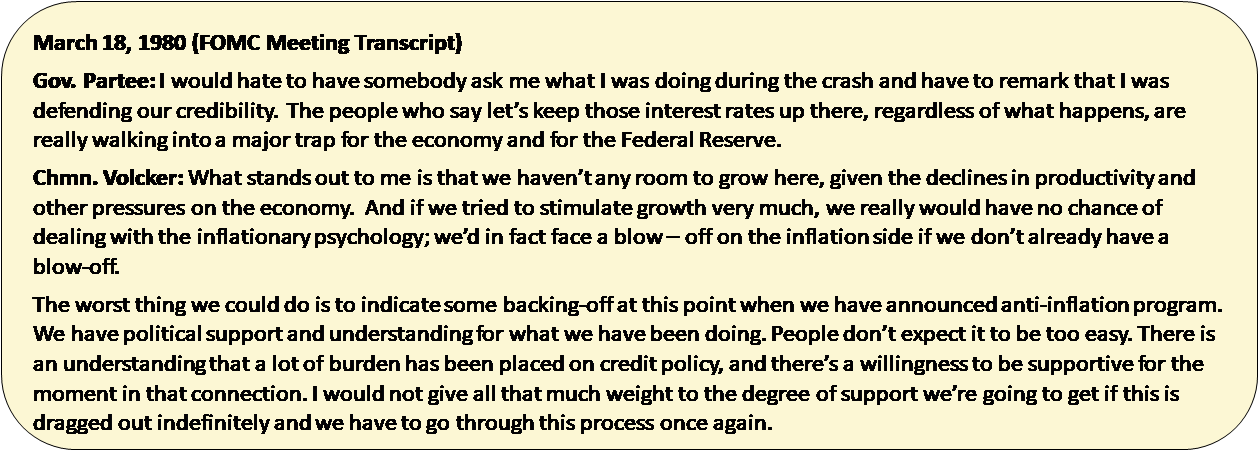

During the first three months of 1980 Volcker held the line on fighting inflation in front of Congress and at FOMC meetings. To both groups, Volcker emphasized the importance of psychology in driving inflation and the need to prove that the Fed could be brave in the face of economic difficulty. The Chairman was able maintain focus on inflation in the FOMC in February and March, but by April the committee had climbed down from its inflation fight and would cut rates until the trough of the recession in July.

Reaganomics, Version the First

Popular narratives frequently date the “Volcker disinflation” from the October 1979 regime change announcement, but the successful implementation of regime change did not actually occur until late 1980 or early 1981. The original inflation fight was abandoned in mid-1980 with the onset of credit controls and a sharp recession in an election year. From the perspective of the public and financial markets the 1979-80 experience was exactly the same as prior inflation-fighting climbdowns where the Fed reacted to sharply rising inflation but backed off once a recession loomed, with political pressure playing a prominent role.

Candidate Ronald Reagan closed the circle left open by Carter’s “malaise” speech in the pair’s final debate before the election of 1980. Reagan’s closing statement in the debate answers the questions and quiets the doubts left festering by the insufficient second half of Carter’s speech. The answer to a lack of confidence was not to ponder the question on television and close with a shrug. Reagan understood that leadership of a free people takes place mostly by example, not by dictate. Reagan’s closing statement was the verbal equivalent of raising Offa’s Sword and declaring the clans united in his personage. The electoral effect was dramatic, and the promise to fight inflation was exactly the signal the FOMC needed to re-launch its effort.

Keep reading with a 7-day free trial

Subscribe to Capitalist Pig Collective to keep reading this post and get 7 days of free access to the full post archives.