Free post: The Weekly Beat: 7 August 2023

See what you've been missing: U.S. Bond Markets, Inflation Watch, Soybeans, and More!

U.S. Bond Market

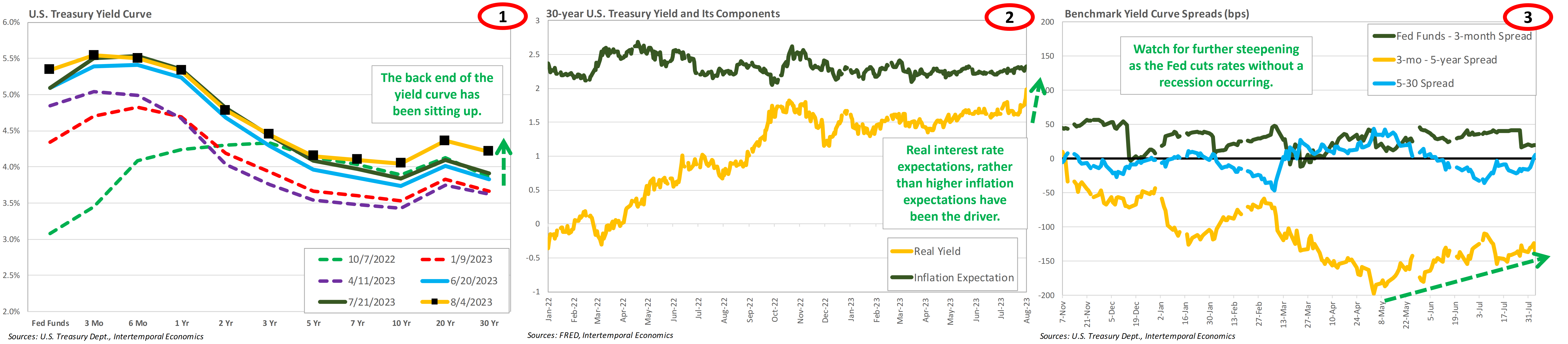

· The back end of the yield curve has been sitting up recently in a so-called “bull-steepening” (Chart 1). Market commentators have attributed the rise to investor capitulation to “tighter for longer” monetary policy being promised by the Fed.

· More likely is that the air is being let out of the long-term bond market as the mix of balance sheet shrinkage and policy rate tightening is being reassessed by the market (Chart 2). During the July FOMC press conference, Powell mentioned the Fed could end up cutting rates while shrinking its balance sheet if inflation were to come down.

· In the second half of this year, this writer is looking for a reversal of the inversion in the middle of the curve as the market increasingly discounts the likelihood of a recession and the Fed cuts rates in reaction to rapidly falling interest rates (Chart 3).

· The reaction to the latest labor market report was a reduction of the expected path of rates as fears of inflationary pressure were reduced. However, the market continues to expect the first rate cut to be delayed into the first quarter of 2024. This writer expects rate cuts to begin sooner than the market’s current expectations. If that were to occur, the two-year rate would also be vulnerable to market surprise. (Charts 4-6)

· Real yields have been pushing higher, likely the result of air being let out of the bond market. We know that the Fed is watching real rates as defined by the bond market very closely. Powell has said that the FOMC is aiming to manage policy with the goal of maintaining a constant level of real rates. (Charts 7-9)

· However, as discussed in recent notes, there is an important mismatch between real interest rates as defined by bond markets versus those perceived by households. This has important implications for strategies involving gold, see below for further discussion.

· Positioning implied by these views are to be long December fed fund futures (ZQZ23) or long the two-year U.S. Treasury (ZTH24, UTWO).

Inflation Watch

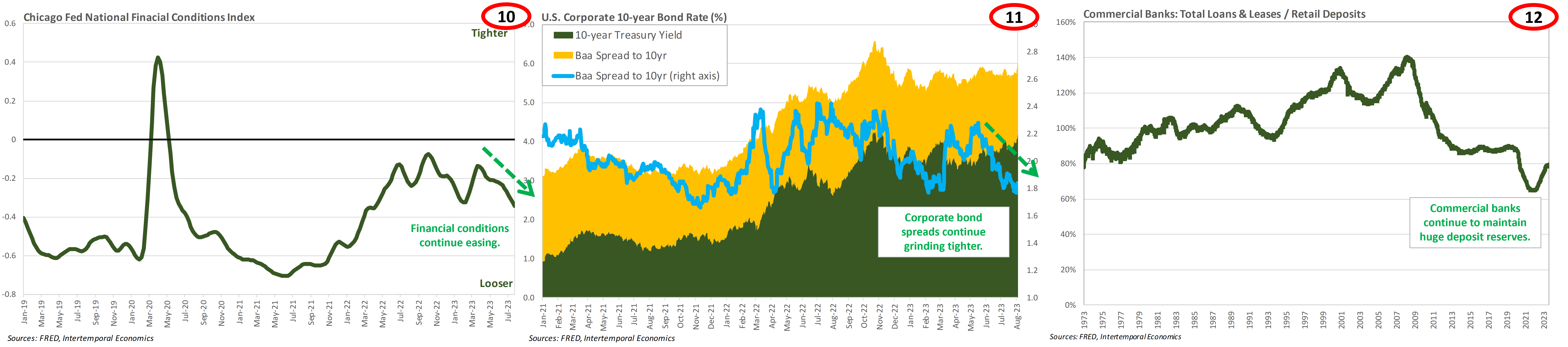

· Credit conditions continue to ease in the U.S. with corporate bond spreads tightening and plenty of deposit funding available for banks (Charts 10-12). This credit expansion is setting up another wave of inflation in 2024, and the earliest signs of the next wave are just becoming visible.

· The Boom/Bust index has spiked recently, caused by a spike in commodity prices, which we can expect to begin affect prices if it is not soon reversed. However, as the Fed always likes to remind us, the volatile headline index is for the mercurial hoi polloi to worry about. Right-thinking people look to the core inflation measure for guidance, and this will be the source of the Fed’s folly in the second half of 2023. (Charts 13-15)

· The state of business on the supply chain and in Chinese factories is abysmal as the aftershocks of the pandemic and the sudden need to pay working capital costs for inventory wreak havoc. Right on schedule, the effect is showing up in the beloved core inflation measure, which should begin to plummet in the coming months. This will give doves on the FOMC much-needed threat to back-up their warnings of a policy overshoot. (Charts 16-18)

Market Positioning

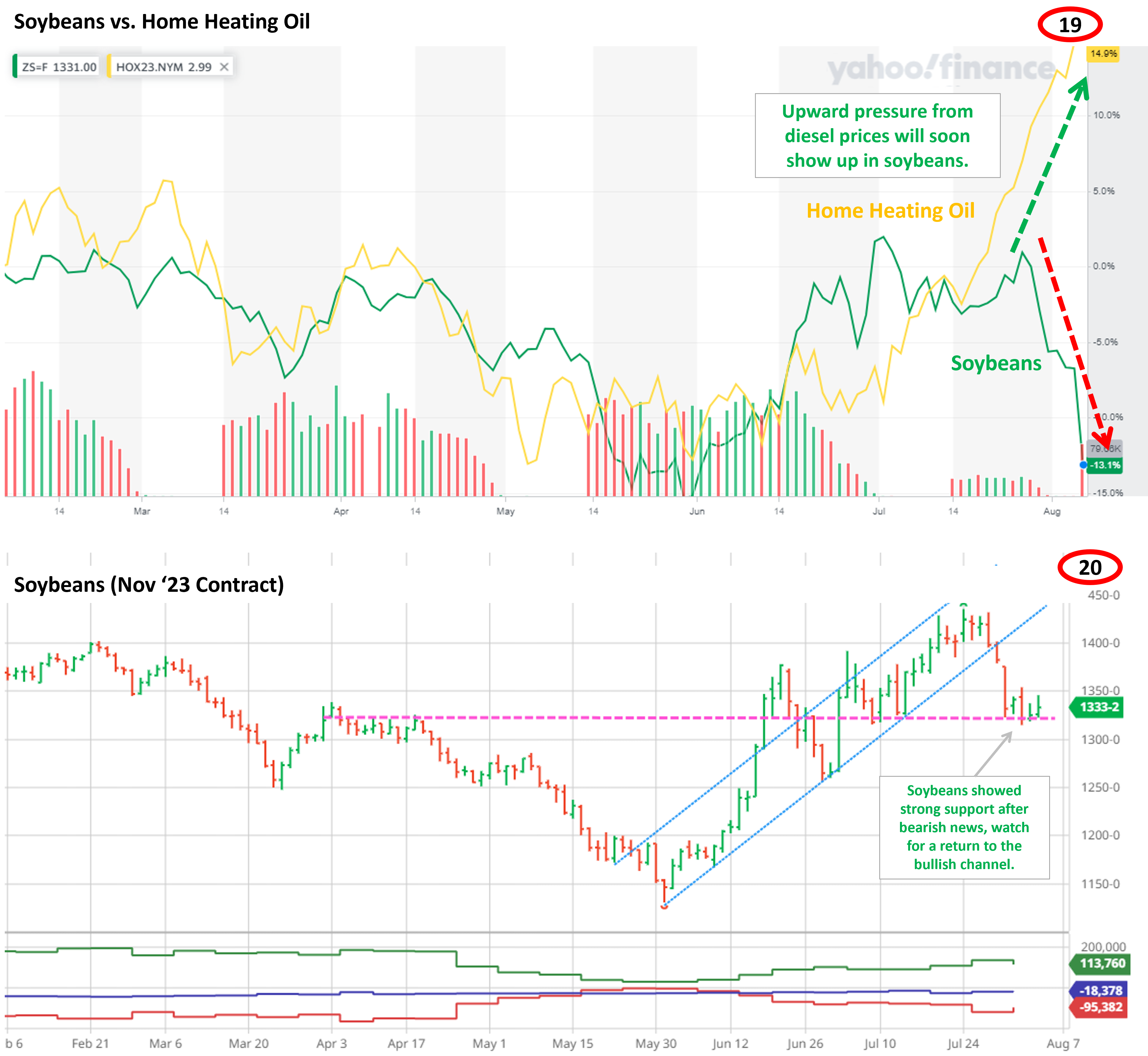

· Soybeans continue to lag diesel fuel, but this situation cannot last long and the volume of renewable diesel production is not sufficient to bring down the price of petroleum diesel. However, the reverse is true, and the current crop yield remains in question as prior drought might have damaged crops. This writer sees long ZSX23 or SOYB as superior to the diesel trade, given the movement in diesel that has already taken place. (Charts 19-20)

· Gold has shown remarkable resilience against rising real rates and has reacted to monetary inflations caused by bank bailouts prior to price inflations. Clearly gold has a lot to offer as long-run protection against the coming waves of inflation. However, over the next six months the Fed is likely to be managing policy using real interest rates as a guide, which puts serious limits on volatility on gold, if successful. An upcoming note will discuss using options trades to cash-in on gold in the near-term, despite the Fed’s efforts to manage real interest rates. (Charts 21-23)