Inflation, Inventories, and the Fed

Trading time for credibility

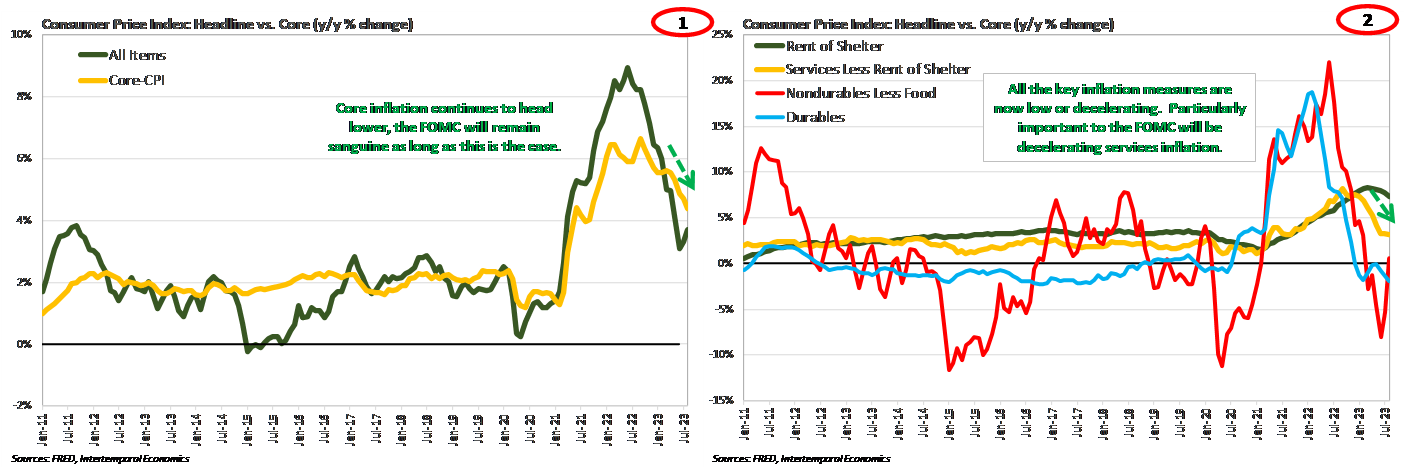

· The continuing decline in core inflation is likely to keep the FOMC sanguine, even as other measures show a boiling point is close at hand.

· The median measures of short-run and long-run inflation expectations look spectacular, and FOMC members will likely take solace in these measures. Although median inflation expectations have been reverting to their long-term averages, the average level of inflation expectations has steadily been moving higher.

· Bottom Line: Lagging headline measures of inflation will continue to send false signals to a willfully ignorant FOMC as inflationary pressure boils away just underneath the surface for the remainder of 2023. Unwilling to raise rates and trigger a recession in an election year, the FOMC will begin to sing the “transitory” tune once again and will trade credibility for time. By mid-year the pressure to act will become too much to resist and the FOMC will begin a belated tightening campaign.

The Good (News)

The stars are aligning nicely for Jerome Powell and the FOMC…well…. if you restrict your view to headline measures of inflation and ignore all other measures. The committee has tied itself to the mast of headline inflation measures with its new operating framework. As a result, the continuing decline in core inflation is likely to keep the FOMC sanguine, even as other measures show a boiling point is close at hand (Chart 1). Particularly pleasing to FOMC members will be the decline in services inflation (Chart 2).

At the headline level, inventories appear to be giving the “all clear” signal to policymakers. Retail inventories excluding motor vehicles are back to 2019 level in aggregate and motor vehicle inventories have been recovering steadily as production bottlenecks are resolved (Chart 3). However, beneath the aggregate measure, it becomes clear that the supply chain remains fragmented and disjointed. Nondurable inventories are still relatively low and durable inventories are relatively high, so nobody is in their sweet spot (Chart 4). Worse yet, the recent labor disruption is likely to drive a deterioration in motor vehicle inventories before they fully recover.

The Bad (News)

The bad news for the FOMC, though they will ignore it, is that the underlying inflation pressure is starting to make itself clear. The recent decline in core inflation has been driven by the inventory overbuild that peaked in early 2023, which is now steadily working itself out. Right on schedule with the turn in inventory pressure has been a turn in Chinese factory prices. Lag effects will result in falling core inflation through the end of 2023, but this is a stale measure that does not reflect growing inflationary pressure (Charts 5-7).

Keep reading with a 7-day free trial

Subscribe to Capitalist Pig Collective to keep reading this post and get 7 days of free access to the full post archives.