On the Knife Edge

An inflation-friendly monetary policy regime

· All signs point to a steady slowing of inflation over the next several months without a recession occurring. Everyone will breathe a sigh of relief, risk assets will outperform, and the Fed will provisionally declare “mission accomplished”.

· Fed staff projections imply they expect the committee to choose inflation above target rather than a recession as the means to balance supply and demand until potential output catches up. We are decidedly in an inflation-friendly monetary policy regime.

The September FOMC meeting minutes included a little-noticed but important statement that “the level of output was expected to be slightly above potential at the end of 2025 [emphasis mine].” That statement means the neutral rate of growth will be negative until 2026 unless economic activity declines and does not immediately rebound. The projection for a negative neutral rate of growth has been a feature of the FOMC minutes in 2022 and the timeline has gotten significantly longer as the year has progressed. In early 2022 the Fed staff projected growth would be above potential until early 2023 and the projection for negative neutral growth has now been pushed out to 2026.

It is worth emphasizing that the statement quoted does not necessarily mean there will be zero growth between now and 2026. Rather, it means that potential output will take over three years to overtake actual output based on the Fed’s assumed growth rates for each. With the policy rate at neutral the rate of growth should be such that inflation trends towards the target rate of two percent. Given the starting point for this exercise is actual output above potential output, setting the policy rate at neutral would put output on a negative trajectory until potential output surpassed actual output. At that point positive growth could commence with the policy rate set at neutral.

If the Fed staff expect actual output to exceed potential output until 2026 it means they expect the FOMC to dance on the knife edge just below the neutral rate such that actual output continues rising but slower than potential growth. The staff projections imply they expect the committee to choose inflation above target rather than a recession as the means to balance supply and demand until potential output catches up. We are decidedly in an inflation-friendly monetary policy regime.

Is There a Draft in Here?

Measures of inflation have been decelerating recently but inflationary pressure is not gone. When supply is tight in general the economy lives on a steep Phillips curve slope (Chart 1). Small changes in the balance of supply and demand will create large swings in the rate of price growth – not prices themselves. That situation is made worse by the distending of the supply chain that took place during the pandemic. With backlogs in transportation and production across the supply chain, the usual symphony of just-in-time inventory has turned into a cacophony of operational chaos.

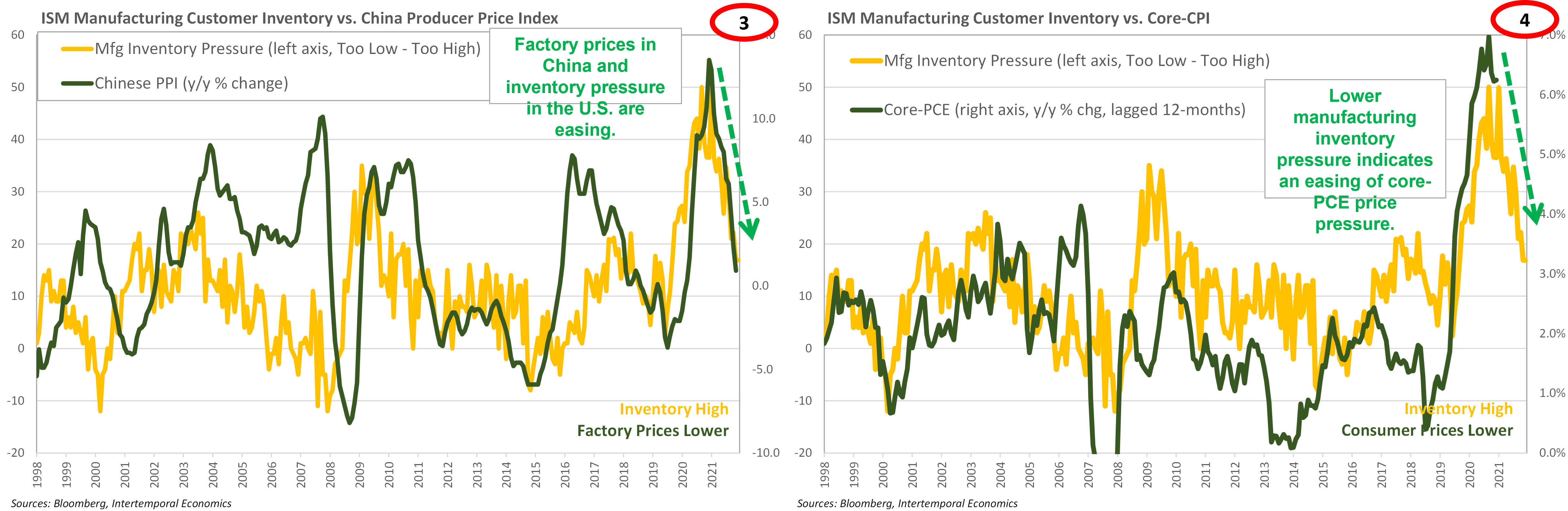

Smooth transmission of inventory signals across the supply chain can no longer be assumed. Case-in-point is the ISM Manufacturing survey results for customer inventories. The percentage of companies reporting customer inventories as ‘too low’ is falling fast while the percentage reporting inventories being ‘too high’ is getting uncomfortably high (Chart 2). The rapid swing in the inventory situation has major implications for inflation when the Phillips curve is steep.

The manufacturing sectors of the China and the U.S. remain tied at the hip with pricing information being transmitted between the two in real time. The current decline in inventory pressure in the manufacturing sector has been met with a deceleration in factory prices in China (Chart 3). The stability of the relationship between the two manufacturing sectors implies the same will be true of the effect on core inflation over the next twelve months (Chart 4). With inventory pressure easing more rapidly than manufacturers expected, the economy is about to exit a hot flash and realize just how cold the room is.

Conclusion

All signs point to a steady slowing of inflation over the next several months without a recession occurring. Everyone will breathe a sigh of relief, risk assets will outperform, and the Fed will provisionally declare “mission accomplished”. However, either one of three things will then occur.

Once the Fed declares victory over inflation credit markets will likely start to flow again. That will raise the temperature of the economy and a rapid return to overheating will occur. Alternatively, another shock to energy prices would create a jolt of inflation that would reduce real interest rates, which would stimulate activity and generate a return to inflation.

In a downside scenario, the current policy rate is already above the rate that would trigger liquidation for many of the bad investments made since the last bubble popped. In that case we will rapidly swing from inflation to deflation, which will force the Fed to ease. However, if the Fed gets a “V” shaped recovery we will be right back where we started – uncomfortably close to potential output and vulnerable to inflation spikes. Each time inflation builds and the FOMC is forced to stomp, the risk of a liquidation scenario rises.

For inquiries about institutional subscriptions simply reply to this email.

Loved this more nuanced read on the CPI report and how things could play out going forward. Thanks!