September FOMC Meeting Recap

Obligatory homage

Comments

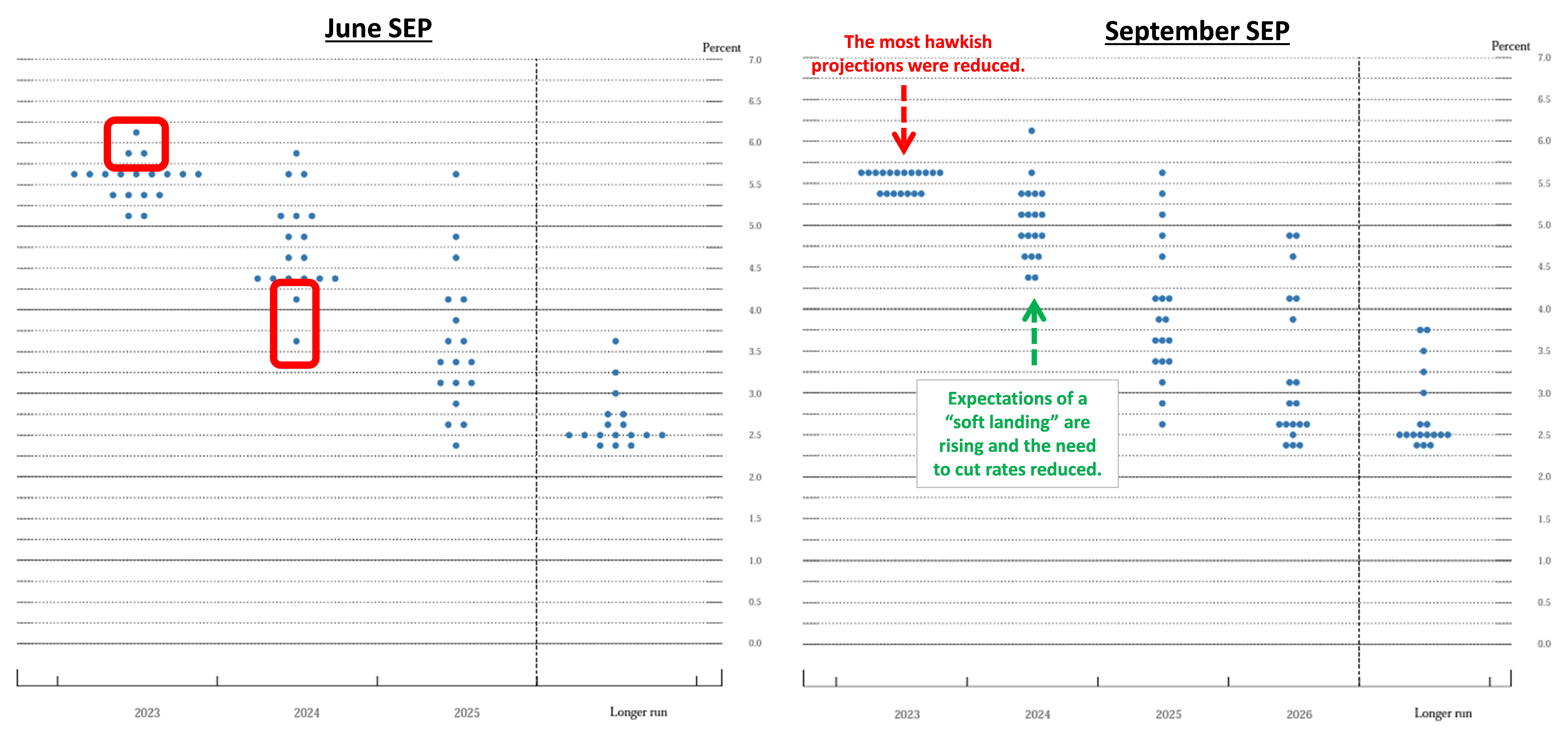

Yesterday, Chairman Powell gave yet another press conference where the obligatory homage was paid to price stability and, once again, market participants labelled the conference as “hawkish”. Playing a key role in driving the “hawkish” narrative in the media was the increase in rate expectations for 2024. During the Q&A Powell was asked whether the increase in rate expectations was due to inflation persistence, but he firmly put that notion to rest. The rate “increases” in 2024 were not driven by higher inflation expectations, but rather diminished expectations that the committee would be cutting rates in response to a recession. More importantly, the outliers who expected to see fed funds above 5.75% by year end 2023 are gone from the projections.

If anything, the repeated references to “proceeding carefully” and the insistence that a soft landing was “the primary goal” made it clear the committee is excitedly anticipating a soft landing and is nervous about losing the game in what it sees as the closing minutes of the match. Powell’s statements were an effort to keep the focus on whether a single hike would be necessary, which he said was economically meaningless, in an effort to avoid discussions about when the cutting starts. The press was already peppering the Chairman with questions about whether rate cuts would be made to keep real interest rates stable. Powell demurred on these questions to avoid prematurely easing via expectations, but he certainly did not say no.

The discussions about risks becoming more “two sided” raises the potential for a small rate cut at the end of 2023, just before inflationary pressure becomes obvious. This writer is watching for a policy error on the dovish side.

Prepared Remarks

Looking ahead, we are in a position to proceed carefully in determining the extent of additional policy firming that may be appropriate. Our decisions will be based on our ongoing assessments of the incoming data and the evolving outlook and risks.

Nevertheless, the process of getting inflation sustainably down to 2 percent has a long way to go.

We see the current stance of monetary policy as restrictive, putting downward pressure on economic activity, hiring, and inflation. In addition, the economy is facing headwinds from tighter credit conditions for households and businesses.

Given how far we have come, we are in a position to proceed carefully as we assess the incoming data and the evolving outlook and risks. Real interest rates now are well above mainstream estimates of the neutral policy rate, but we are mindful of the inherent uncertainties in precisely gauging the stance of policy.

We are prepared to raise rates further if appropriate, and we intend to hold policy at a restrictive level until we are confident that inflation is moving down sustainably toward our objective.

Question & Answer

Q: So right now, it's still an open question about being sufficiently restrictive. You're not saying today that we've reached this level?

CHAIR POWELL. No. Clearly what we decided to do is maintain the policy rate and await further data. We want to see convincing evidence, really, that we have reached the appropriate level, and we're seeing progress, and we welcome that. But we need to see more progress before we'll be willing to reach that conclusion.

Q: How would you characterize the debate around another hike or holding steady? Is it discussion around lag times, fear of too much slowing, too little slowing? Could you walk us through what this disagreement was about at the meeting?

CHAIR POWELL. Yeah, so the proposal at the meeting was to maintain our current policy stance, and I think there was obviously unanimous support for that. But I think people, they want to be convinced, you know, they want to be careful not to jump to a conclusion really one way or the other, but just be convinced that the data, you know, support that conclusion. And that's why, given how far we've come and how quickly we've come, we're actually in a position to be able to proceed carefully as we assess the incoming data and the evolving outlooks and risks and make these decisions meeting by meeting.

A year ago, we proceeded pretty quickly to get rates up. Now we're fairly close, we think, to where we need to get. It's just a question of reaching the right stance. I wouldn't attribute huge importance to one hike in macroeconomic terms. Nonetheless, you know, we need to get to a place where we're confident that we have a stance that will bring inflation down to 2 percent over time.

Q: Does the Committee believe inflation to be more persistent, requires more medicine effectively?

A: It's more about stronger economic activity, I would say. If I had to attribute one thing, I think broadly stronger economic activity means we have to do more with rates, and that's what that meaning is telling you.

I think broadly, people still think that there will have to be some softening in the labor market. That can come through more supply, as we've seen as well. Also, remember the natural rate we think is coming down, which is a supply-side thing, so that the gap between any given unemployment rate that's lower than that and the natural rate comes down, that's a way for the labor market to achieve a better balance.

Q: Would you call the soft landing now a baseline expectation?

A: No, no. I would not do that. I would just say -- what would I say about that? I've always thought that the soft landing was a plausible outcome, that there was a path, really, to a soft landing. I've thought that and I've said that since we lifted off. It's also possible that the path is narrowed, and it's widened apparently.

Q: Is the FOMC focused on targeting a real level of policy restriction? And can you explain what would constitute enough evidence that will allow the FOMC to normalize the nominal stance of policy while keeping real policy settings sufficiently restrictive?

A: I mean, yes, we understand that it's a real rate that will matter and that needs to be sufficiently restrictive. And, again, I would say you know sufficiently restrictive only when you see it. It's not something you can arrive at with confidence in a model or in various estimates, you know.

We want to reach something that we're confident gets us to that level. And I think confidence comes from seeing, you know, enough data that you feel like, yes, okay, this feels like we can for now decide that this is the right level and just agree to stay here. We're not permanently deciding not to go higher, but let's say if we get to that level. And then the question is, how long do you stay at that level? And that's a whole other set of questions. For now, the question is trying to find that level where we think we can stay there. And we haven't gotten to a point of confidence about that yet.

Q: What if GDP stays hot, but without inflation?

A: So I think the question will be, GDP is not a mandate, right? Maximum employment and price stability are the mandates. The question will be, is the heat that we see in GDP, is it really a threat to our ability to get back to 2 percent inflation? That's going to be the question. It's not a question about GDP on its own.

Q: Is a soft landing not an objective?

A: To begin, a soft landing is a primary objective, and I did not say otherwise. I mean, that's what we've been trying to achieve for all this time. The real point, though, is the worst thing we can do is to fail to restore price stability, because the record is clear on that. If you don't restore price stability, inflation comes back, and you can have a long period where the economy is just very uncertain and it will affect growth, it will affect all kinds of things. It can be a miserable period to have inflation constantly coming back and the Fed coming in and having to tighten again and again. So the best thing we can do for everyone, we believe, is to restore price stability. I think now, today, we actually have the ability to be careful at this point and move carefully, and that's what we're planning to do.

Q: Given the forecast that you have, what justified not moving today, and what could justify moving in the future if you think inflation is coming down? In other words, why did you leave that extra dot in?

A: Well, I think we have come very far very fast in the rate increases that we've made. And I think it was important at the beginning that we move quickly, and we did. And I think as we get closer to the rate that we think, the stance of monetary policy that we think is appropriate to bring inflation down to 2 percent over time, you know, the risks become more two-sided. And the risk of over-tightening and the risk of under-tightening becomes more equal. And I think the natural, common-sense thing to do is as you approach that, you move a little more slowly as you get closer to it. And that's what we're doing. So we're taking advantage of the fact that we have moved quickly to move a little more carefully now as we sort of find our way to the right level of restriction that we need to get inflation back down to 2 percent.