The Political Economics of Student Loan "Forgetfulness"

A bubble is a bubble...

The human capital investment bubble funded by government education loans is no different than the land bubble funded by government guaranteed mortgages. Cheap credit was provided to newly “eligible” borrowers who were the least prepared of all other adults in society to manage credit.

Government-provided student loans are a perfect Keynesian lever to boost consumption and I expect politicians will increasingly utilize them as a policy tool. In the near-term look for small-scale easing of terms if growth slowdown concerns increase and should be viewed as a source of upside risk for inflation. However, the big payoff will come when there is a serious downturn.

I use the term “forgetting” rather than “forgiving” when considering the ultimate solution for the student loan issue because of political realities. Unless Bernie Sanders becomes President there will be no “forgiveness”, but whether borrowers carry so-called loans on their balance sheet is irrelevant. What matters is whether anyone (especially private sector lenders) expect those loans to be paid back. Shifting political sentiment determines who feels the pain of funding higher education.

Note to readers: First, apologies for the slow flow of notes. I was under the weather this week but hope to get caught up soon. Second, this note was distributed to Premium Plus clients on March 19, 2019. It builds on a note distributed to Connolly Insight readers in 2013. I am distributing it on Substack because the topic is a timely one, but also to showcase what my research methodology.

I make high conviction calls using economic first principles that have long lead times. Unfortunately, that method has not generated much interest on Wall Street, where short-termism is the religion of choice. My work has been much more popular in the UK where thinking is still in fashion. I’m hoping the broader global audience and Americans who don’t work on Wall Street will value my work more than the U.S. financial sector has.

Buying Friends

A little-noticed, but politically and economically important, event took place in late 2018. The net flow of cash to the household sector via the US Federal government’s student loan scheme flipped to negative. Net principal flows are still running at nearly $90 billion annually in favor of the household sector, but net interest payments have caught up (Chart 1). Uncle Sam is about to go from “The First Bank of Partying” to “The Hangover Inquisitor”. Labor market strength has accelerated the process by reducing the outflow of principal as undergrad enrollment has fallen and graduate student enrollment has ceased growing (Chart 2). Higher income will offset the rising net burden of course, but this note is about the political pressure on Washington DC to “do something” about the unpleasant reduction in consumption needed to pay back the student loan binge. The political prize for avoiding the Great Payback Hangover will simply be too great to pass-up in the midst of a bitter partisan struggle for power.

A significant number of words have been written about how much education debt is owed, but when the debt is held by politicians a more important consideration is who owes the debt. College-educated nonwhites are a reliable source of votes and donations for Democrats, but college-educated White voters are battleground (Charts 3,4,5). This has especially been the case in the Age of Trump, much to the distress of Senate Republicans. Finally, as will be discussed below, the average age of student loan borrowers is rising rapidly and is currently shifting from the 30s range to the 40s. This is a key age range because these are the years where voters begin to shift to favoring Republicans over Democrats. Clearly, Democrats will be looking to change that Republican advantage among older voters.

Distribution of Balances and Performance

Student loans in the US are political debt that are widely owed (45 million Federal Direct Loan borrowers) and cut across demographic groups. Student loan borrowers are a cornucopia of votes made up of various interest groups presenting a variety of needs. As far as the politicians are concerned, there is something in the trough for everybody.

Note how massively lopsided outstanding balances are across borrower types. Twenty-five million borrowers owe less than $20,000 each, but a mere 2.7 million owe in-excess of $100,000 each (Chart 6). However, those 2.7 million high-balance borrowers owe more than twice the aggregate balance of low-balance borrowers.

Adding to the complexity is that borrowers with massive balances are the least likely to default (Chart 7). Indeed, among borrowers who owe less than $5000, over the life of the loan 20% will default, an additional 17% will experience a 120+ day delinquency period and an additional 8.5% will experience an out-of-school negative amortization period.

College students with the time and willingness to put on costumes and hold signs get most of the attention in media reports, but the true weight of the debt burden is on those in their 30s and 40s (Chart 8). This age demographic is where most of the debt is owed, and most borrowers are concentrated. Most college students owe less than $50,000 of Federal loans at graduation due to borrowing limits. That is not the case for graduate students who are eligible to borrow up to the full cost of tuition and fees, school supplies and living expenses (Chart 9). The balances stack up fast and 1.7 million borrowers in their prime earnings years owe an aggregate of nearly $300 billion. These borrowers are a political prize primarily because of the donations they provide, but also because professionals are a key voting demographic in the suburban battlegrounds that lay between the urban strongholds of the Democrats and the rural domains of the Republicans.

Three primary factors are driving the divergence in debt balances among undergraduate and graduate student borrowers. As discussed above, the divergence in enrollment among undergrads and graduate students is part of the reason. Another is borrowing limits on undergrads, which has simply shifted marginal borrowing onto parents.

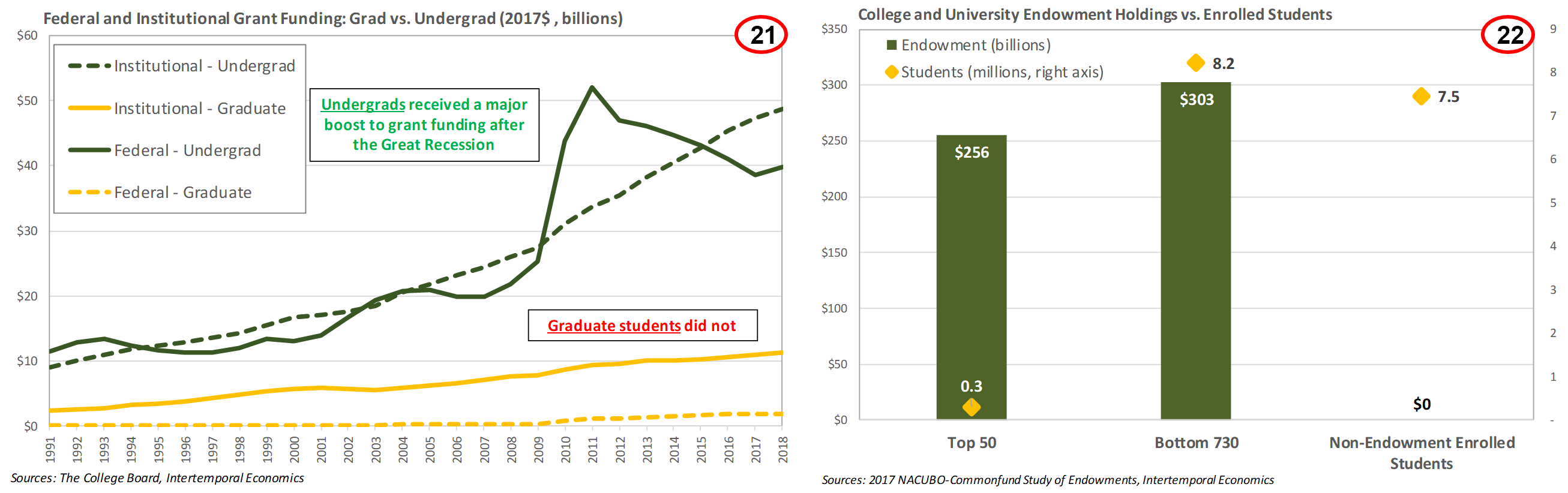

A third factor has been that shifting funding sources and political pressures have led older borrowers who were undergrads in the 2000s and graduates in the 2010s to be hit by a double whammy of student debt. In the lead-up to the Great Recession the rising cost of higher education drove a massive increase in undergrad borrowing (Chart 10). That process went into overdrive when unemployed workers fled to school and funded their time out of the labor market with cheap and readily available student loans. Since the recession, a jump in grant funding has driven down borrowing per student and severely depressed borrowing in the private student loan market.

Unfortunately for graduate students, the same boost in grant funding never occurred and student loan borrowing filled the funding gap (Chart 11). These same students, who were slammed with undergraduate debt in the 2000s have been hit with graduate school debt in the 2010s. The charts below the stark age-split in the debt-load. Shifting political sentiment determines who feels the pain of funding higher education.

The Politics of Forgetfulness

Politicians casting about for reasons to justify avoiding asking for full repayment of student loans will be delighted to find plenty of Keynesian arguments available. A widely acknowledged truism that college graduates with student debt (i.e. their future earnings are leveraged already) have less available space on their balance sheet for other assets (i.e. homes and autos). As a result, homeownership for those who have student debt is lower than those without such debt (Chart 12). In addition, student loans are rising as a share of consumer durable investment and will begin to cut into funding more fun durable investments (i.e. cars and other recreational vehicles) (Chart 13). Memories of college ten years ago are cold comfort for those struggling to fund a car loan due to student loan payments.

As mentioned above, a key political consideration for student loans is the aging of borrowers into battleground demographics (i.e. voters in their late-30s and 40s). Falling enrollment and a flood of free money has halted rising balances among younger borrowers, but all other demographics are experiencing rapidly rising aggregate balances (Charts 14,15). Indeed, borrowing by parents has tripled in inflation-adjusted terms since 1990. There are nearly 4 million Parent PLUS loan borrowers and parent borrowers are not eligible for borrower protections (i.e. unemployment deferral) or income-driven repayment plans. Credit standards for parent loans are atrociously loose. Borrowers can be delinquent on up to $2,000 of government loans and still qualify for additional loans. Credit eligibility was weakened in 2014, which made government loans available to an additional 370,000 (and rising) borrowers.

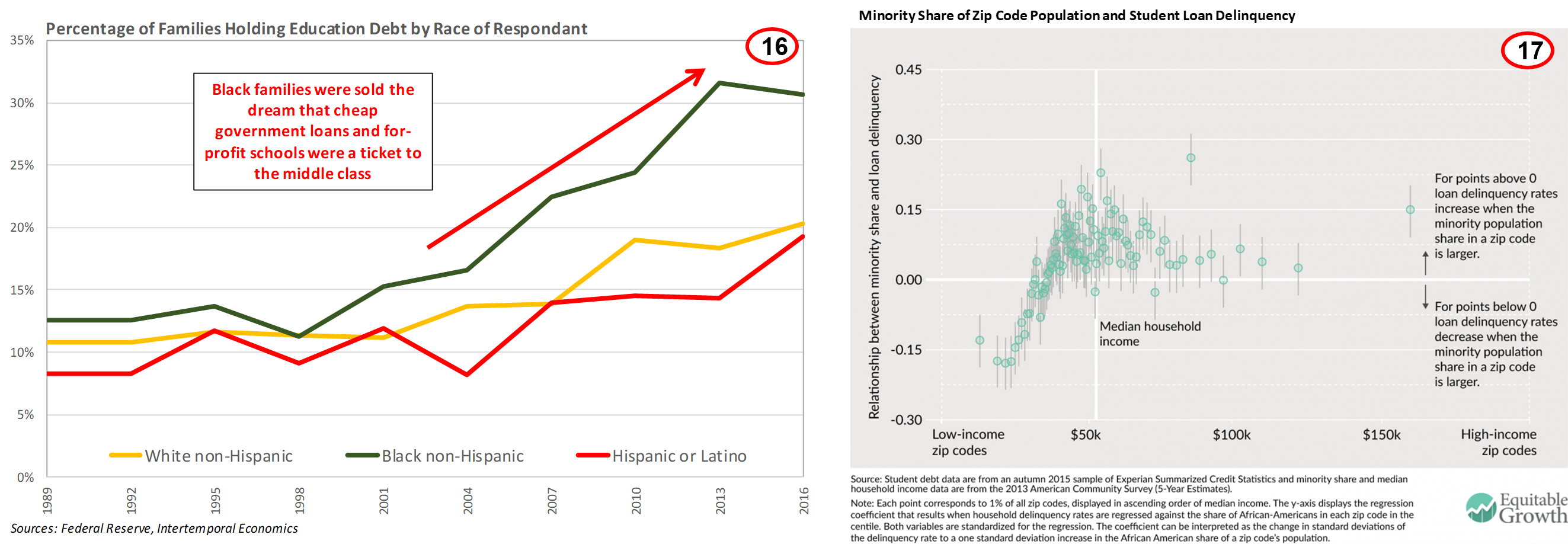

For Democrat politicians, Black voters are a critical voting base that is in desperate need of relief from student loan burdens. Black families have been sold on the concept that a college education is an automatic ticket to the middle class. Since the mid-2000s black families have leveraged for human capital investment significantly more than Whites and Latinos (Chart 16). The result has been blacks, particularly those in middle-income brackets, have disproportionally defaulted on their student loans (Chart 17).

If low-income students, particularly Blacks, had entered non-profit institutions at the same rates as higher-income students the situation might have turned out much differently (Chart 18,19). Unfortunately, the reverse occurred and the (higher proportion of) low-income Black students at for-profit schools leveraged drastically during and since the Great Recession (Chart 20). Actual income for these students turned out to be significantly lower than expected, particularly for the many who are listed as “some college”. Most of the borrowers in this category are dropouts.

The debate over for-profit colleges and universities that plays out in the media generally focuses on the small number of large publicly traded for-profit schools. Although borrowers from these schools experience higher default rates than those at non-profit schools, a much greater problem is the thousands of small for-profit professional schools. Indeed, many are simply “schools” run out of existing businesses who enroll fewer than 10 students. These types of schools experience atrocious default rates. Indeed, the 2015 default rates for Cheryl Fell’s School of Business and Champ’s Barber School were 47% and 58% respectively. Among schools with the 100 highest default rates, 65 are for-profit and 38 of those are beauty/barber/cosmetology schools.

Forgetting the Loans

I use the term “forgetting” rather than “forgiving” when considering the ultimate solution for the student loan issue because of political realities. Unless Bernie Sanders becomes President there will be no “forgiveness”, but whether borrowers carry so-called loans on their balance sheet is irrelevant. What matters is whether anyone (especially private sector lenders) expect those loans to be paid back. If I owe you more of my lifetime consumption than I am willing to give up and you never demand I pay you back… Do I really owe a debt? God bless you if you answered yes, because in my opinion the vast majority of borrowers will be more than happy to “forget” about the debt they owe you.

Forgetting the debt is the only viable method of reducing the outstanding debt-load and arresting further balance accrual. The easy sources of cash have been tapped out and budgeting rules in the US Congress make it much easier to fund programs where money never comes in rather than an equivalent amount of cash going out the door. The boost to undergrad grant funding was driven by funding from the Federal government and the schools themselves. Sending out more money will be difficult for Congress until there is a serious downturn and only a small minority of schools have cash to throw around. The top 50 assets-per-student endowments (excluding religious schools) hold nearly half of the endowment assets ($256 billion) out of the nearly 5,000 colleges and universities in the US. These schools enroll about 300,000 students. Another 730 schools with 8.2 million enrolled students hold $303 billion. Seven and a half million students attend non-profits with no endowments or for-profit schools.

Cash out the door will not be an option except in a serious downturn and an immediate and wide-spread forgiveness will simply be out of the question politically for Republicans and even a few Democrats. Fortunately for the politicians, an alternative and relatively painless path to forgetting the loans has already been laid out.

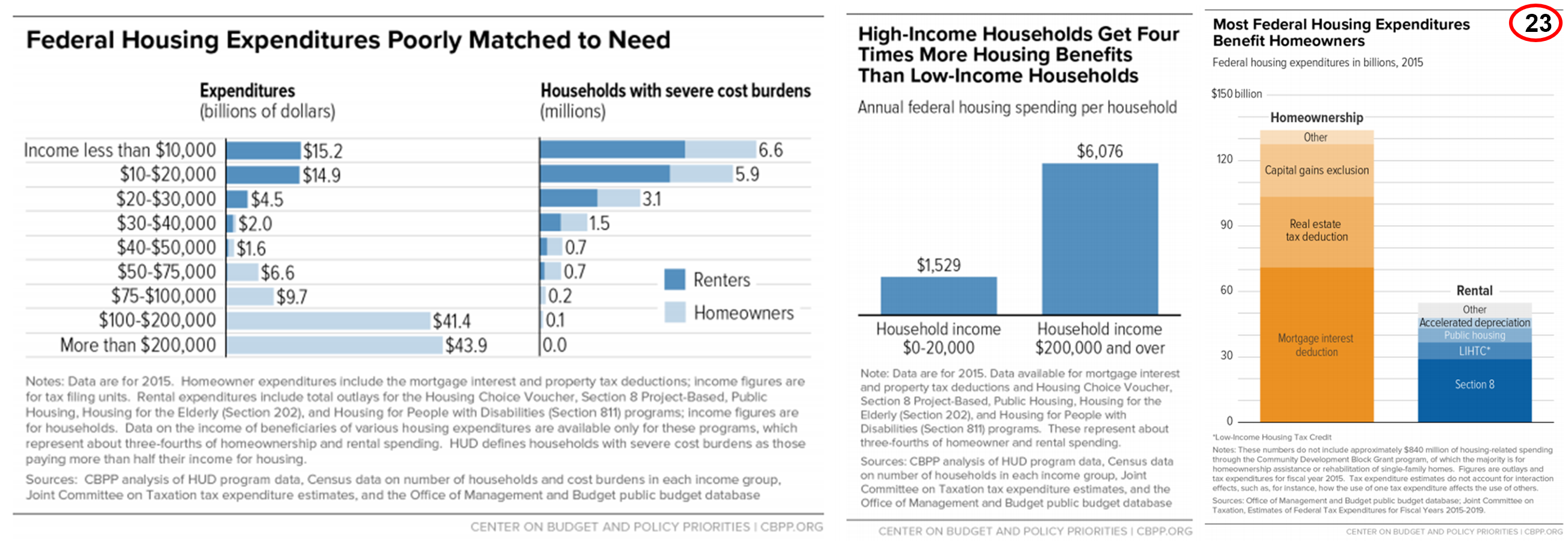

In my opinion, the models for dealing with Federal student loans are already laid out in the government’s homeownership and back-door welfare schemes. An income bracket barbell strategy is clearly displayed in the tax and credit policy for housing. Low interest rates and mortgage interest deductions provide subsidies for above-average income “homevoters” (Chart 23). At the bottom of the income spectrum are Section 8 housing subsidies, food-for-work subsidies (i.e. SNAP) and free-money-for-working payments (i.e. the refundable Earned Income Credit). These programs provide small-dollar cash payments to subsidize the living standards of the working-poor and are a pet patronage system for Democrats.

As discussed above, millions of borrowers owe less than $5,000 dollars. The debts of these borrowers will likely be partially forgotten via refundable tax credits for on-time payments by low-income borrowers. For low-balance borrowers the cash payments will be small enough to fit into the overall welfare scheme.

High balance borrowers, especially those in middle-income brackets who have lower tax bills, are a harder nut to crack from a political standpoint. They owe too much to hand out the cash and, in most cases, could realistically reduce consumption sufficiently to pay the loans back without being reduced to a life of destitution. But that does not matter because the lender is the government, which can be compelled (or bribed) to ignore the original intention of lending money and being paid back. Indeed, a transfer system is already in place because the Federal Direct loan program loses 16 cents for every dollar of loans made.

The process for providing debt avoidance to student loan borrowers in the middle-and upper income brackets is already well-underway. The process only needs to be expanded and accelerated (with the budget recognition pushed beyond the statutory 10-year horizon) to provide a rapid economic boost by increasing household free cash flow and reducing expected lifetime payments via forgiveness schemes.

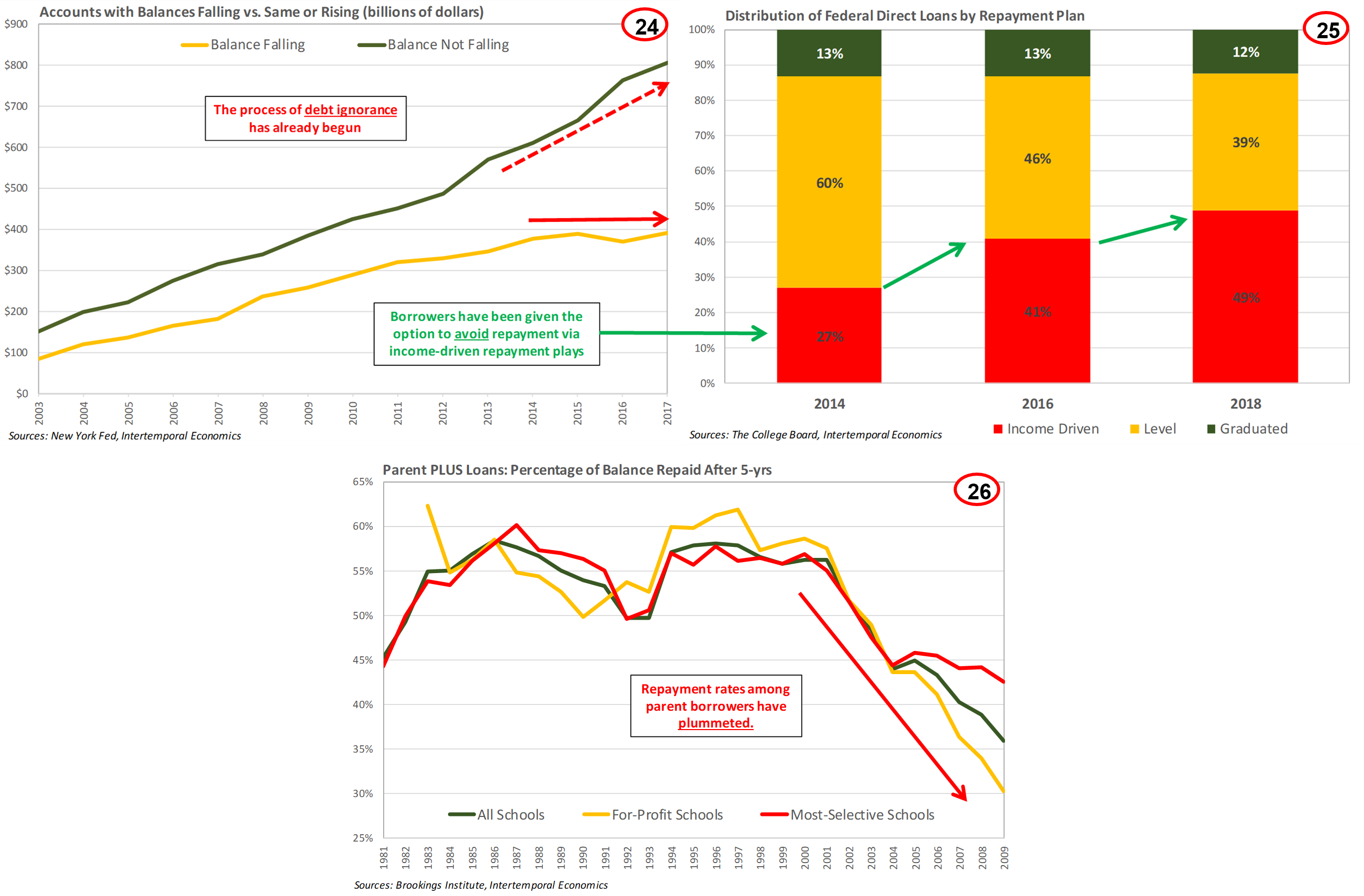

A series of new increasingly generous “income-driven” repayment plans were rolled out during the Obama years. These plans limit total payments (i.e. income and principal) to 10% of gross-adjusted income above 150% of the poverty line. The payment maturity schedule is stretched out indefinitely and the outstanding balance is forgotten after 240 on-time payments (120 for public sector workers). Thus, the payment horizon is undefined, meaning the outstanding balance can continue rising indefinitely, and the date for extinguishing the loan is well-before the expected repayment date. Indeed, from the borrower’s standpoint the expected repayment date might not exist at all in such a high moral-hazard environment. As mentioned above, the forgetting process is already well-underway. Two-thirds of outstanding balances are in accounts where the balance is not falling (Chart 24). Only 18 million borrowers out of a total of 45 million is actually in repayment status.

In addition, the share of borrowers enrolled in income driven repayment plans (with debt extinguishment provisions) has been rising rapidly and I expect will become the default option set by the government (Chart 25). I would argue most borrowers entering these programs are not expecting to pay these balances back, especially ultra-high balance borrowers.

Avoidance of education loans is most-definitely not confined to young-adults making poor decisions. Parent-borrower repayment rates have plummeted since the early 2000s, particularly for parents of students at for-profit schools (Chart 26). Is it realistic to expect a 62+ year old borrower to pay fifty thousand dollars or more over a twenty-year time horizon? I think not.

The incentive to shift to an income-driven forgetfulness scheme becomes clear once you look at non-performance data by repayment schedule. A plurality of borrowers in-repayment are enrolled in repayment schedules with level payments and a “short-dated” maturity of ten years (Chart 27). In contrast, a significant majority of balances are enrolled in income-driven programs with balances limited to a set portion of adjusted income. Not surprisingly, the repayment plans with payments limited to a set portion of income have lower nonperformance rates and the more generous the program, the lower the nonperformance rate (Chart 28).

Income-driven repayment schedules are an easy mitigant for the pain of student loan repayments. These programs require no further legislation and, in all seriousness, the time horizon for accounting for debt extinguishment is beyond the expected lifespan for most US Senators. For those in the House of Representatives a twenty-year time horizon is likely a lobbyist gig. If borrowers act as if the money will not be repaid, private lenders feel the same way and Ricardian Equivalence is not operating, then balances can continue rising without any brake on consumption. The transversality constraint has been negated by political considerations[1].

High-income borrowers enrolled in income driven repayment programs might actually be required to pay back their entire balances under current rules if their incomes grow fast enough. But look at the situation from a political point-of-view. High income borrowers have managed to pay their student loan balances back in the past but think of the honeypot available for everyone at the top of the social order. If I was a politician, I’d be willing to bet that a good portion of the newly-available free cash flow will go to consumption and investment, but out of a trillion dollars even a small portion allocated to political donations is big bucks.

As with the maturity extension solution, an upper-income tax scheme is already in-place and only needs to be expanded. Borrowers with incomes above $75,000 now received 40% of federal tax credits for education in 2016, up from 25% in 2006 (Chart 29). Much of the boost was directed at undergraduate students and their parents. Plenty of room exists to expand graduate student tax benefits to match undergrad tax credits, as was the case before 2008 (Charts 30,31).

Who Really Pays?

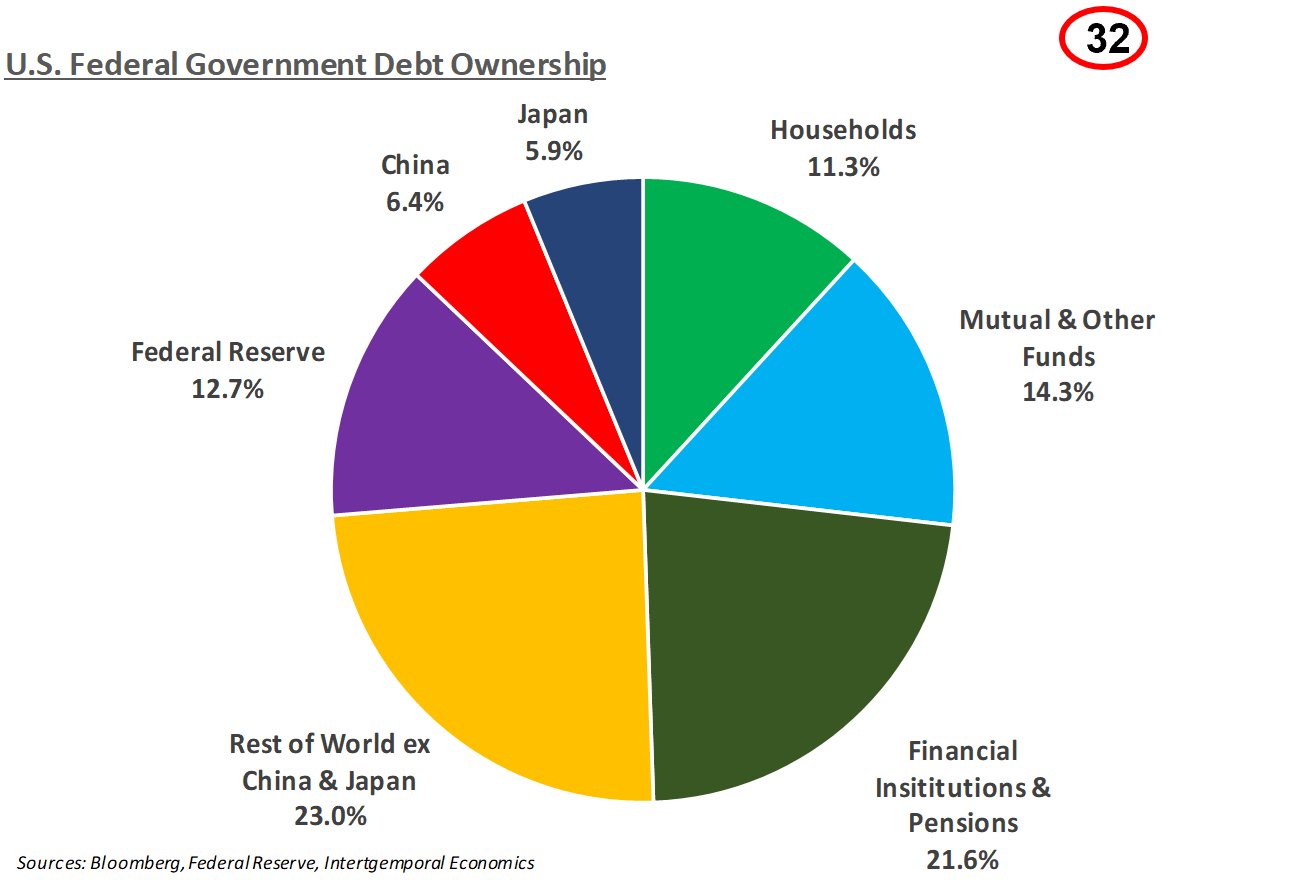

A concern/complaint heard frequently by this writer is that student loan “forgiveness” will be foisted off onto “the taxpayer”. However, it is worth considering whether this is really the case. A majority of federal debt is held for regulatory, monetary policy, private-sector “money” creation[1] or other motives that require perpetual “risk-free” debt (Chart 32). Again, if debt is never repaid, is it really debt? I’m not arguing that an expanding the federal debt-load indefinitely would no negative economic or financial effects. But in the relevant timescale repayment will not be demanded and there are plenty of uses other than storing value or generating income for Treasury bonds – especially with negative yielding Bunds and JGBs. With no Ricardian Equivalence the household sector will interpret forgetfulness student loan balances as an opportunity to boost consumption.

In my opinion, the place to go looking for outright loan forgiveness is at the state government level. In a post-industrial economy where healthcare and education costs are rising rapidly, an ample supply of highly-educated professionals are crucial for a successful local economy. States have already begun the battle for professionals and the tax dollars they bring via generous student loan relief programs[1]. One example is Maryland’s attempt to draw professionals working in the Washington DC metro area (including the tech hubs in Herndon and McClean, Virginia) away from the Virginia suburbs. Maryland will forgive up to $30,000 of student loan debt of first-time home buyers. Watch for states programs to grow where metro-areas span state boundaries – New York City is an obvious example.

Conclusion

Obviously, the probability of a “wave of the hand” amnesty that makes $1.4+ trillion dollars of education debt disappear is effectively zero. But that is not necessary if everyone acts as if the debt is contained (i.e. a twenty-year tithe) and that – as has been the case thus far – terms of repayment can only be expected to ease further. Readers might be tempted to point to Trump’s proposed budget, which drastically cuts student loan forgiveness programs. However, under American rules the President’s budget proposal is purely an exercise in domestic politics. The President can feed highlights to his base and signal quietly to Congress initiatives he’s willing to venture political capital on. As discussed above, 63% of Trump voters were non-college whites. He cannot very well come out and give out handouts to low-income minorities and urban professionals. However, I’d argue he’ll be happy to sign anything that comes along with funding for any type of physical barrier for the border (velvet purple rope with faux gold banisters, maybe).

The big giveaway will be a refinancing at zero percent and further limitation on either (or both) the percentage of income paid per year, or the share of income exempted from the “adjusted income” calculation. Indeed, Democrats have proposed increasing the exemption from 150% of the poverty line to 250%. With a specific benefit for “small business owners” (and Mitt Romney) for the Republicans to hang their hats on the deal will be done. Refinancing will require a serious downturn with 10-year rates flirting with zero percent. The important point is that Congress has a variety of ways to ease the terms of education loans that can avoid explicit recognition in current budgets. The Department of Education has been most helpful in avoiding repayment by consistently grossly underestimating the cost of easing loan terms. Indeed, the DoE expected income-driven forgiveness to cost $1 billion per year until 2020 but is currently running near $15 billion.

Skeptics of my viewpoint point to the scale of student loan interest and principal flows relative to overall consumption. No doubt total consumption is vastly larger than consumption funded by government loans, but that is completely irrelevant from an economic analysis viewpoint. The important aspect of student loan growth is that credit expansion generated higher consumption growth than would have otherwise been the case. Not only were the effects marginal in an expenditure sense, but also in the credit quality of borrowers. As was the case during the housing bubble, an arbitrary form of investment was assumed to be a guaranteed ticket to the middle class. Cheap credit was provided to newly “eligible” borrowers who were the least prepared of all other adults in society to manage credit. The human capital investment bubble funded by government education loans is no different than the land bubble funded by government guaranteed mortgages. Finally, the annual cash flows are much less important than the lifetime net present value of future payments. If private lenders and borrowers agree to leverage this newly “found” money, there could be a significant boost to consumption that occurs very rapidly.

Government-provided student loans are a perfect Keynesian lever to boost consumption and I expect politicians will increasingly utilize them as a policy tool. In the near-term look for small-scale easing of terms if growth slowdown concerns increase and should be viewed as a source of upside risk for inflation. However, the big payoff will come when there is a serious downturn.

[1] See my Connolly Insight note “Euler, Transversality and Intertemporal Disequilibrium” of 11 November 2016

[1] See my Connolly Insight note “Money (That's What I Want)” of 18 October 2013.

[1] See: https://thecollegeinvestor.com/student-loan-forgiveness-programs-by-state/