The Weekly Beat: 19 December 2022

ManHawkDove, Gold is Shiny, Travelling Container Glut

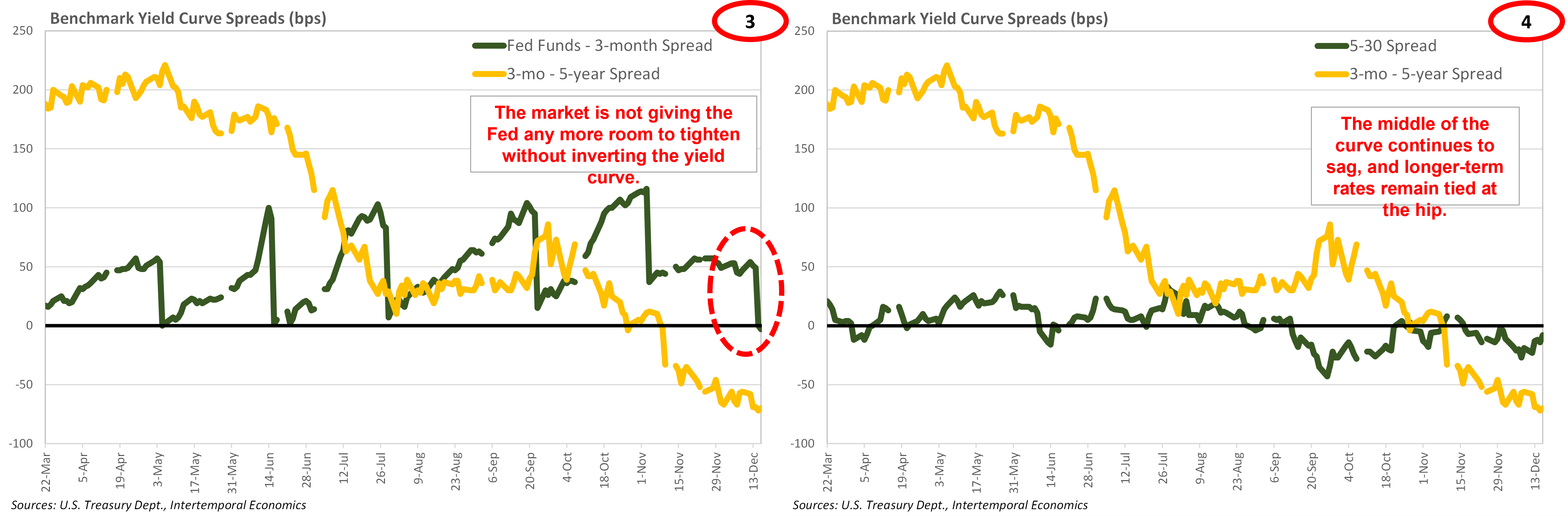

U.S. Bond Markets

· The overnight lending rate responded to the FOMC’s policy decision last week, but the rest of the yield curve was indifferent. Indeed, since Biden declared victory over inflation on November 10th bond yields have steadily fallen.

· The Fed has effectively run out of room to tighten as the front of the yield curve is flat, the middle is downward sloping, and the back end is flat. Additional policy rate increases will definitively invert the curve and make a recession unavoidable.

· Real rates did not respond to the Fed’s supposedly hawkish statement but have been trending down since early November. Powell did his best to talk up the long end of the curve by discussing the FOMC’s expectations that policy would remain restrictive for “some time”, but the market didn’t bite. See below for highlights from the presser.

· Despite Powell’s numerous assertions during the press conference that the Fed would not repeat the mistakes of the 1970s, the Fed’s current policy stance is remarkably like Fed policy during that period. He says that “reducing inflation is likely to require a sustained period of below-trend growth and some softening of labor market conditions” but a recession will not be necessary to rebalance the economy.

· On close examination Powell’s statements on the need for restrictive policy were much less definitive than appear at first glance. Powell says that the committee plans to slow down rate increases to “feel our way” to the terminal rate of policy tightening. He also said “we've continually expected to make faster progress on inflation than we have”.

· Since the Fed’s forecasts have been so bad as inflation was rising, they could well be mistaken on the downslope as well. The Fed could very well find itself “behind the curve” going into a disinflationary period, prompting an unscheduled easing.

· Powell clearly laid out conditions needed to cease tightening and, eventually, put easing on the table. He said, “But there's an expectation that the services inflation will not move down so quickly, so that we'll have to stay at it so that we may have to raise rates higher to get to where we want to go.” So a sudden weakening of service sector wages, or even a deterioration of business conditions would get the FOMC thinking about being less restrictive.

· Financial markets are eyeing an end to tightening with financial conditions easing generally and corporate bond spreads tightening. High yield issuers are closed out of the market, but investment grade issuers have had no trouble selling paper. With some surety on where rates will be in a year, lenders will open up and start lending their pile of deposits.

· Gold held up surprisingly well against rising real rates during 2022. The correlation between gold and real rates remains, but a level shift took place in gold. As fears of inflation grow in coming years there are likely to be more of these level shifts where rising real interest rates squeeze out some long holders, but the price never comes back to its former range.

Canadian Bond Markets

· The bad news continues in Canadian bond markets as the yield curve remains badly inverted and markets are pricing in more pain. Canadian money markets, unlike their U.S. counterparts, are betting on further tightening moves by the Bank of Canada. Like the U.S., expectations of disappointing future growth are weighing on bond yields further out on the curve.

· Given the discrepancy between the overnight rate and the three-month rate, the market appears to be signaling to the central bank that a policy error has occurred. Also like the U.S. market, yields at the long end of the curve have been locked together.

In the News: Watch for the Upturn

Decaying demand sees China's ports building empty container mountains

FedEx Freight to begin driver furloughs Sunday

Shipping stocks in the crosshairs as China fears mount

Transportation as an Economic Indicator

Highlights From Powell’s Dec 14, 2022 Post-FOMC Conference

-- We continue to anticipate that ongoing increases will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive... In addition, we are continuing the process of significantly reducing the size of our balance sheet. Restoring price stability will likely require maintaining a restrictive policy stance for some time.

-- Reducing inflation is likely to require a sustained period of below-trend growth and some softening of labor market conditions. Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run. The historical record cautions strongly against prematurely loosening policy.

-- As we lifted off and got into the course of year and we saw the -- how strong inflation was and how persistent, it was very important to move quickly. In fact, the speed, the pace with which we're moving was the most important thing. I think now that we're coming to the end of this year, we've raised 425 basis points this year and we're into restrictive territory, it's now not so important how fast we go.

-- I've told you today we have an assessment that we're not at as restrictive enough stance, even with today's move. At a certain point, though, we'll get to that point. And then the question will be how long do we stay there. And there, the strong view on the Committee is that we'll need to stay there until we're really confident that inflation is coming down in a sustained way. And we think that that will be some time.

-- The third piece, which is something like 55 percent of the index, PCE core inflation index, is non-housing-related core services. And that's really a function of the labor market, largely, at the biggest cost by far in that sector is labor.

-- The goods inflation has turned pretty quickly now after not turning at all for a year and a half. But there's an expectation that the services inflation will not move down so quickly, so that we'll have to stay at it so that we may have to raise rates higher to get to where we want to go. And that's really why we are writing down those high rates and why we're expecting that they'll have to remain high for a time.

-- [H]aving moved so quickly and having now so much restraint that's still in the pipeline, we think that the appropriate thing to do now is to move to a slower pace. And, you know, that will -- that will allow us to feel our way and -- you know, and get to that level, we think, and better balance the risks that we face. So that's the idea.

-- The labor market is clearly very strong. It is more just that, you know, by now, we had expected -- we've continually expected to make faster progress on inflation than we have, ultimately. And that's why the -- that's why the peak rate for this year goes up between this meeting and the September meeting.

-- If you look at wages, look at the average hourly earnings number we got with the last payrolls report, you don't really see much progress in terms of average hourly earnings coming down.

-- So, you know, one thing is to say is I think our policies in -- getting into a pretty good place now. We're restrictive, and I think we're -- you know, we're getting close to that level of sufficient, we think sufficiently restrictive. We laid out today what our best estimates are to get there. And, I mean, it boils down to how long do we think this process is going to take?

-- [Q: Is the soft landing is no longer achievable?] [A: I wouldn't say that. No. I would say this: You know, to the extent we need to keep rates higher and keep them there for longer and inflation, you know, moves up higher and higher, I think that narrows the runway. But lower inflation readings, if they persist in time, could certainly make it more possible. So I just -- I don't think anyone knows whether we're going to have a recession or not and, if we do, whether it's going to be a deep one or not. It's just it's not knowable.]