The Weekly Beat: 28 February 2023

Downside Weights, Hawkish Pauses, and Self-inflicted Sanctions

U.S. Bond Markets

· Minutes of the FOMC’s early February meeting did not provide the disinflation discussion bonanza everyone was looking for, but signs of a turn in policy mindset were plain-to-see regardless. The estimate for potential output to move above actual output was pushed back by a year to the end of 2025, but the economic staff and FOMC participants viewed the risks to economic activity as “weighted to the downside.”

· FOMC members spent time agreeing that current inflation was much too high, but their outlooks were very sanguine and getting back to 2% was viewed as a matter of timing. "Some participants judged that recent economic data signaled a somewhat higher chance of continued subdued economic growth, with inflation falling over time to the Committee’s longer-run goal of 2%, although some participants noted that the probability of the economy entering recession in 2023 remained elevated.”

· Unfortunately, the path back to 1970s inflation is clearly laid out in the discussion of racially based monetary policy. An exchange between the old-school members and Biden’s recent nominees over whether unemployment or inflation is worse for favored economic groups lays bare the divide within the Committee. An upcoming note will explore this topic in detail.

“A number of participants commented on the importance of recognizing that, to the extent national unemployment increases, historical evidence indicates that even larger increases in the unemployment rate for some demographic groups—particularly African Americans and Hispanics—would be likely to occur.”

“A number of participants commented that the costs of elevated inflation are particularly high for lower-income households.”

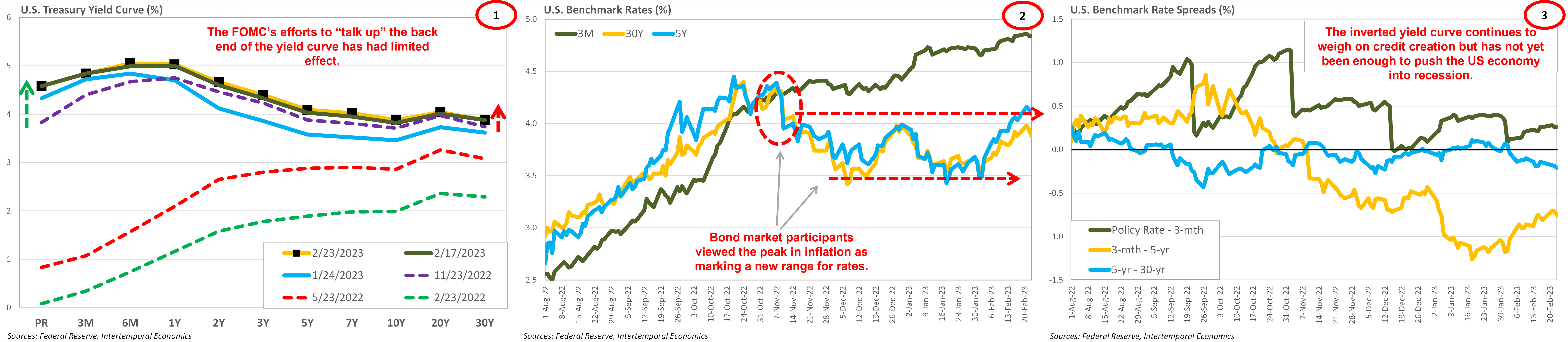

· Board members’ efforts to “talk up” the back end of the yield curve via promises of keeping rates higher for longer have met with very limited success. When inflation peaked in November 2022 and Biden tweeted celebration the bond market moved into a new range and it will take more than just words from the Fed to break that range (Charts 1-3).

· Real rates have settled into a comfortable range as inflation expectations have returned to the Fed’s comfort zone. The market and the Fed have convinced themselves that they are on the glidepath to victory over inflation. The Goldilocks thesis will begin to suck in more and more market participants only to chew them up and spit them out when inflation returns in late 2023 (Charts 4-6).

· The seeds of that next inflation can be found in the ongoing easing of financial conditions that is rapidly erasing much of the tightening that took place in 2022. Undoubtedly, the cost of credit is higher in 2023 than it was in 2022, but the availability has not been sufficiently diminished to cool inflationary pressure (Charts 7-9).

· Data from the supply chain continues to indicate several months of easing inflationary pressure ahead. Indeed, it could be that central bankers will become frightened they’ve gone too far and begin to reverse prior tightening. However, using the 1970s as a guide, inflation will never get back to its prior “too low” levels before accelerating again (Charts 10-12).

G-7 Bond Markets

· Since we last wrote, Bank of Canada Governor Tiff Macklem took on the unenviable task of explaining his bank’s hawkish pause. The fragility of Canada’s housing market forced the BoC to pause rate hikes sooner than the Fed, but the dilemma is one that all of the major central banks will face.

· Indeed, the similarity of the yield curves across the US, UK, and Canada underlines the problem the entire world faces at present. As said by Macklem, “Changes to our policy rate have also affected the exchange rate. But the exchange rate channel has been more muted than usual. Because the US Federal Reserve was also raising rates rapidly through 2022, the Canadian dollar did not appreciate against the US dollar.”

· Most importantly, Macklem says “This fight against inflation is a global one— we’re not fighting it alone. “ It bears remembering that although the Bank of Canada is not currently fighting alone, it is also not fighting in cooperation with the other central banks.

· Only Japan currently benefits from a non-inverted yield curve and the benefits will likely become more pronounced as the Canadian housing market implodes. As inflation makes a comeback in 2023, the central banks of the G-7 will turn to yield curve control for the purpose of competitive currency appreciations.

In the News: Self-Inflicted Sanctions Regimes

Sanctions effect begins: Crude tankers forced onto longer voyages

Russian Urals grade crude that used to go to the EU is now going all the way to India. China is also taking Russian crude, China’s daily oil imports from Russia could increase by as much as 500,000 barrels this year to about 2.2 million barrels. About 400 crude oil vessels, or 20% of the global fleet, have “switched” from mainstream trades to “ostensibly do Russian business,” co-head of oil trading Ben Luckock said in an interview on Bloomberg Television. For oil product tankers, the company sees the level at 200 tankers, or 7% of the world total.

Our Take: Strategic partnership with India, and control of the Arabian Sea and Indian Ocean, are about to rise in value significantly. Watch for growing tensions in the Red Sea as efforts to pressure Russia continue. Meanwhile, Russia and China are likely to extend their military alliance to South Africa in an effort to secure coal and a southern corridor for oil exports. The inevitable battlefield is the open waters that lay between Africa and ASEAN islands.